Note that in our basic balance sheet template, the “Total Assets” and “Total Liabilities” line items include the values of the “Total Current Assets” and “Total Current Liabilities”, respectively. Commercial paper is a form of short-term debt with a specific purpose, different from long-term debt. Since commercial paper is a debt-like security, certain financial models consolidate commercial paper with the revolving credit facility (“revolver”) line item.

Calculating the change in assets of a company

For this example, we’ll use this hypothetical balance sheet of ABC Company, an industrial manufacturer. The table below summarizes the company’s assets for the past two year-end periods. QuickBooks Online users have year-round access to QuickBooks Live Assisted Bookkeepers who can give personalized answers to bookkeeping questions and help manage their finances.

What Is the Balance Sheet Formula?

As the name suggests, the equation balances out, with assets on the one side being equal to the sum of liabilities and equity on the other. Depending on the company, different parties may be responsible for preparing the balance sheet. For small privately-held businesses, the balance sheet might be prepared by the owner or by a company bookkeeper. For mid-size private firms, they might be prepared internally and then looked over by an external accountant. Some companies issue preferred stock, which will be listed separately from common stock under this section. Preferred stock is assigned an arbitrary par value (as is common stock, in some cases) that has no bearing on the market value of the shares.

Part 2: Your Current Nest Egg

These assets are often sold at retirement and can become a part of the retirement portfolio. The personal net worth statement shows personal items owned and amounts owed. Investments are long‐term assets that should generate a reasonable return (over time). They become the backbone of retirement, personal, and business planning efforts.

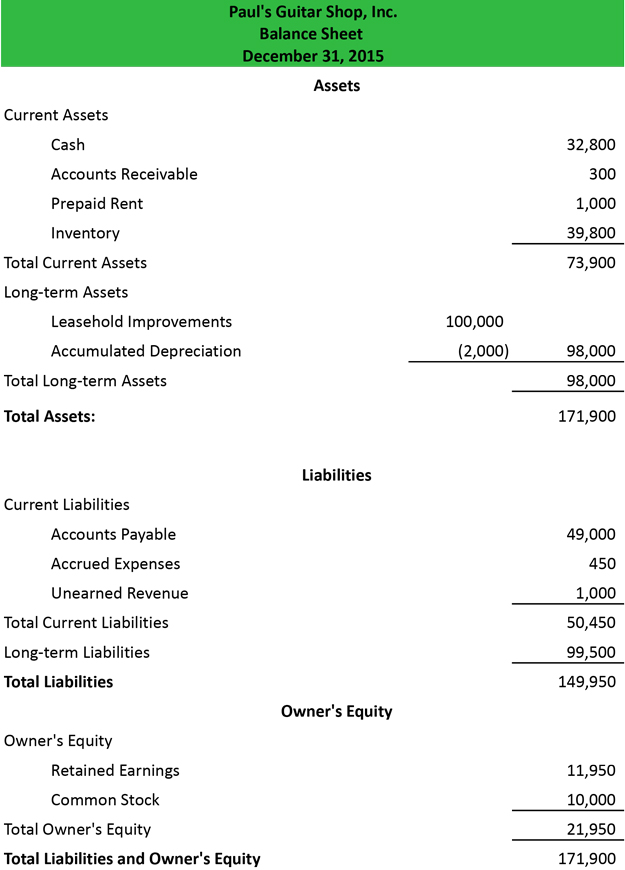

- You can also compare your latest balance sheet to previous ones to examine how your finances have changed over time.

- The first is money, which is contributed to the business in the form of an investment in exchange for some degree of ownership (typically represented by shares).

- Returning to our catering example, let’s say you haven’t yet paid the latest invoice from your tofu supplier.

The balance sheet, income statement, and cash flow statement make up the three main financial statements that businesses use. Companies are required by law to generate these financial statements. Here’s an example to help you understand the information to include on your balance sheet. In the example accounting equations mcq quiz with answers below, we see that the balance sheet shows assets (such as cash and accounts receivable), liabilities (such as accounts payable, credit cards, and taxes payable), and equity. Total liabilities and equity are also added up at the bottom of the sheet—hence the term ‘bottom line’ for this number.

To do this, just divide the difference from above, $420 million, by last year’s total assets, $1.975 billion. Multiply that result by 100 to see the percentage change — in this case, 21.3%. Again, a positive number indicates growth, and a negative number indicates a decline. In this example, take $2.395 billion and subtract $1.975 billion; the result is $420 million. That means that ABC Company increased its total assets by $420 million during this one-year period.

While the balance sheet can be prepared at any time, it is mostly prepared at the end of the accounting period. A balance sheet is meant to depict the total assets, liabilities, and shareholders’ equity of a company on a specific date, typically referred to as the reporting date. Often, the reporting date will be the final day of the accounting period. A company’s balance sheet provides important information on a company’s worth, broken down into assets, liabilities, and equity.

It should not be surprising that the diversity of activities included among publicly-traded companies is reflected in balance sheet account presentations. In these instances, the investor will have to make allowances and/or defer to the experts. The information found in a company’s balance sheet is among some of the most important for a business leader, regulator, or potential investor to understand. The balance sheet is used to assess the financial health of a company. Investors and lenders also use it to assess creditworthiness and the availability of assets for collateral. Balance sheets include assets, liabilities, and shareholders’ equity.

A balance sheet captures the net worth of a business at any given time. It shows the balance between the company’s assets against the sum of its liabilities and shareholders’ equity — what it owns versus what it owes. The financial statement only captures the financial position of a company on a specific day. Looking at a single balance sheet by itself may make it difficult to extract whether a company is performing well. For example, imagine a company reports $1,000,000 of cash on hand at the end of the month.

The image below is an example of a comparative balance sheet of Apple, Inc. This balance sheet compares the financial position of the company as of September 2020 to the financial position of the company from the year prior. In business a reputation for keeping absolutely to the letter and spirit of an agreement, even when it is unfavorable, is the most precious of assets, although it is not entered in the balance sheet. We can add context to this number by calculating the percentage change during the period.

A company should make estimates and reflect their best guess as a part of the balance sheet if they do not know which receivables a company is likely actually to receive. For instance, accounts receivable should be continually assessed for impairment and adjusted to reveal potential uncollectible accounts. Again, these should be organized into both line items and total liabilities. This will make it easier for analysts to comprehend exactly what your assets are and where they came from. Tallying the assets together will be required for final analysis.